Warren Buffett Buys REITs Instead Of Real Estate, Here’s Why

Warren Buffett is one of the very few investors to have managed to compound returns at a 20% annual average for more than 50 years.

Anyone can succeed over a 5-10 year time period, but the real test is whether you can keep going for decade after decade, and Warren Buffett’s Berkshire Hathaway (BRK.A) (BRK.B) is one of the rare exceptions to have achieved that:

| Berkshire Hathaway | S&P 500 (SPY) | |

| Compounded Annual – 1964-2020 | 20.0% | 10.2% |

| Overall Gain – 1965-2020 | 2,810,526% | 23,454% |

So, when he talks, we listen.

In today’s article, we look closer at his approach to real estate investing. Over the years, he has often discussed why he rarely buys real estate, but more recently, he has made large investments in the REIT sector (VNQ).

Below we highlight five reasons why Warren Buffett favors REITs over private property investments:

Reason #1: No Competitive Advantage

In a shareholder meeting decades ago, Warren Buffett explains that they are not equipped to compete with investors who specialize in real estate investing.

The interesting thing here is that back then Warren Buffett already had invested millions into real estate, had significant resources through Berkshire, and Charlie had made his initial fortune in real estate.

Even then, they felt that they couldn’t compete with REITs and other LPs that specialized in real estate investing and had an informational edge over them.

Here you should ask yourself: If Warren and Charlie cannot compete in the real estate space, can you?

A lot of individual investors think that after watching a few YouTube videos and buying a real estate investing course from an online guru, they’re well prepared to become real estate investors.

In reality, most investors are overconfident and overestimate their abilities. Warren Buffett is very realistic about his limitations and understands that unless you are 100% focused on real estate, you’re unlikely to achieve good results investing in it.

Reason #2: Lack of Mispricing

Somewhat related to reason #1, if you are not fully dedicated to real estate, you are unlikely to find mispriced opportunities.

Warren Buffett explains that mispricings in real estate are rare. The market is relatively efficient at pricing risk because most investors are long-term oriented.

On the other hand, mispricings are more frequent in the stock market because most investors are short-term-oriented and quick to panic when they see their stock decline in value.

Warren believes that if you are an active investor, you’re more likely to find better deals in the stock market, including REITs, than in private real estate.

That’s what he said years ago and it is well reflected in today’s market.

Right now, housing is red hot, and commercial real estate is selling at historically low cap rates. The prices reflect the ultra-low interest rate environment that we live in.

Even then, the REIT market is today severely mispriced. Many REITs, including blue-chip names like W.P. Carey (WPC), Realty Income (O), and National Retail (NNN) are down by 20-30% even as their underlying properties are more valuable than ever before.

That’s a better opportunity.

Reason #3: Corporate Tax Disadvantage

Berkshire Hathaway is structured as a corporation and it’s liable to corporate taxes.

Charlie and Warren explain that this puts them at a major disadvantage relative to REITs, which are exempt from corporate taxes.

If you earn a 6% yield on a property, the REIT is left with 6%, but Berkshire is left with a lower profit due to taxes.

Even then, Berkshire has made REIT investments, which are more tax efficient because REITs only pay out 50%-70% of their cash flow in dividends, and the rest is retained at the REIT level and not taxed. Moreover, REITs have a greater growth/appreciation component than private real estate, which results in lower corporate taxes.

Reason #4: Management And Scalability

In an interview during the great financial crisis, Warren Buffett explains that if he had a way to efficiently manage real estate, he would load up on single-family homes.

A lot of investors make the mistake of assuming that real estate is a passive investment when in reality it can be management intensive.

You are dealing with the dreaded 3 Ts: Tenants, toilets, and trash.

Could Warren Buffett hire a property management company? Sure, he could. In fact, he would get a much better deal than you or me if he did that.

However, the issue with property management companies is that their fees eat into your profitability, but even more importantly, their interests are not aligned with yours. Buying a property and handing the keys to a property manager is the equivalent of buying an externally-managed REIT, which we all know, is rarely a good idea due to conflicts of interest.

With traditional REITs, Warren Buffett gets professional management that’s well aligned with shareholders and enjoys significant economies of scale.

You also can easily deploy capital in a few clicks of a mouse, which makes it easy to scale your investments over time.

Reason #5: Opportunities are in REITs Today

Warren Buffett is a value investor.

He wants to buy high-quality assets at a discount to fair value.

But as noted earlier, the private real estate market is currently red hot. With the exception of a few challenged sectors (office, malls, etc.), you’re unlikely to find discounted opportunities. The demand for private real estate is greater than ever before due to the ultra-low interest rates.

Even then, many REITs are today priced at historically low valuations, and not surprisingly, that’s what Warren is buying. Below we highlight one of his favorite REITs:

STORE Capital

Berkshire Hathaway first bought shares of STORE Capital (STOR) back in 2017, and recently, they doubled down.

As a result, they now own nearly 10% of the equity:

According to an interview of Chris Volk, CEO of STORE Capital, it’s Warren Buffett that was behind this investment. You can skip to the 8:55 mark to learn more about Warren Buffett’s investment in STORE:

What’s so special about STORE Capital?

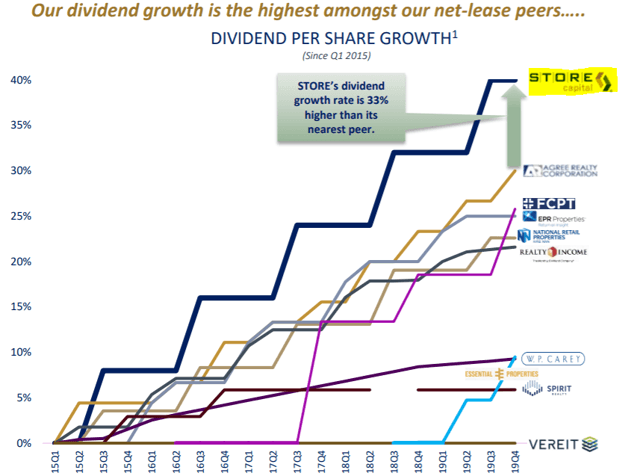

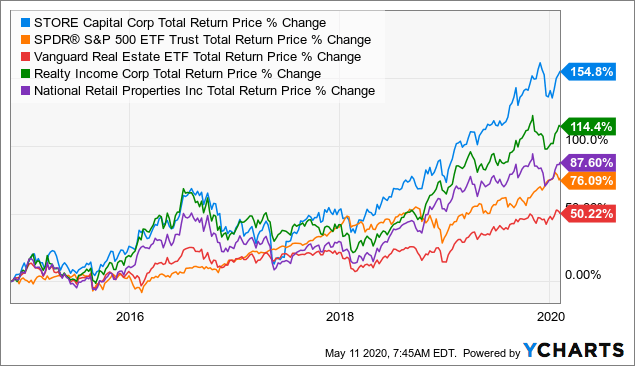

In short, STOR has a unique strategy that generates higher returns with lower risk than what Berkshire could achieve on its own. We discuss this strategy in detail in a separate article so we won’t go into the details here, but its strategy has consistently led to significant outperformance relative to its close peers, and this is likely to continue far into the future:

Even then, STOR has been priced at an exceptionally low valuation over the past year. It’s still ~15% lower than prior to the pandemic, and that’s despite hiking its dividend by 3% in 2020 and guiding for record-high cash flow in 2022.

You simply cannot find this type of opportunity in the private real estate market and that’s why Warren Buffett favors REIT investments.

Today, there are ~25 similar REIT opportunities in which we are investing at High Yield Landlord.

")